How to Withdraw USDT to a Bank Account Safely: Fees, Limits, and Step-by-Step Process

This blog post will cover:

- Introduction: Why Safe USDT Cash-Out Matters in 2025-2026

- Understanding USDT and Bank Withdrawals

- Main Ways to Withdraw USDT to a Bank Account

- Fees Explained: What You Really Pay When Cashing Out USDT

- Withdrawal Limits, KYC, and Compliance Requirements

- Step-by-Step Process: Withdrawing USDT to a Bank Using SimpleSwap

- Risk Management and Safety Best Practices

- Optimization Tips: Saving on Fees and Time

- Tax and Reporting Considerations

- Key Takeaways and Practical Checklist

- FAQ

Introduction: Why Safe USDT Cash-Out Matters in 2025-2026

The rise of USDT as a cash-out asset

By 2025, USDT has quietly become the default "cash leg" of the crypto market. Traders, freelancers, and long‑term holders park profits in Tether, treat it as working capital, and move in and out of USDT whenever they need to cover rent, payroll, or day‑to‑day expenses. Because it tracks the dollar and sits at the center of so many trading pairs, shifting from volatile coins into USDT often feels like stepping to the sidelines without leaving crypto entirely.

That behavior is reshaping how people think about withdrawals. Instead of cashing out Bitcoin or altcoins directly, many now convert to USDT first and only then look for the cleanest route from USDT to their bank.

Who this guide is for and how SimpleSwap helps

This guide is aimed at three main groups: people withdrawing USDT for the first time, active traders who regularly skim profits into fiat, and freelancers or small businesses that invoice in Tether and then need to pay real‑world bills. Despite very different profiles, they tend to worry about the same things: which route is actually safe, what the full cost will be, and whether their bank might question a crypto‑linked payment.

On one side, the guide provides the conversion layer that takes USDT from your wallet and routes it into assets that can be paid out through regulated partners. On the other, it tries to strip away the mystery-spelling out options, limits, and common pitfalls so each USDT cash‑out feels like a planned transaction instead of a guess.

Understanding USDT and Bank Withdrawals

Why you can't send USDT directly to a bank account

One of the first surprises for new users is that you can't just "send USDT to your bank" the way you wire dollars. Your bank only deals in fiat currencies such as USD or EUR, and its internal ledger has no idea what to do with tokens that live on Ethereum, TRON, or any other blockchain. USDT exists entirely on those crypto networks; your checking account exists entirely inside your bank's own system.

To turn USDT into money you can swipe or wire, someone has to stand in the middle, sell that USDT for fiat, and then push the proceeds through traditional rails like ACH, SEPA, or SWIFT.

One may explain that as connecting two different "tracks": the crypto track (where you send USDT from your wallet) and the banking track (where compliant, traceable fiat payments move between institutions). An exchange, off‑ramp, or payment processor bridges those tracks for you. Once you see it as a two‑step process-on‑chain transfer, then fiat payout-it becomes much easier to compare options and spot where things might slow down or cost more.

Key players in a USDT cash-out transaction

Every time you cash out USDT, a small cast of characters gets involved, even if an app makes it look like one click. It starts with you, holding USDT in a wallet or on a platform and deciding you'd rather see money in your bank balance. Next comes the conversion layer: a centralized exchange, a non‑custodial service like SimpleSwap that plugs into liquidity providers, or sometimes a P2P marketplace. That middleman receives your USDT on‑chain, converts it into fiat, and passes control of the payout to a bank or payment processor.

From SimpleSwap's vantage point, the flow typically looks like this: your USDT wallet sends funds to a SimpleSwap address, SimpleSwap and its partners execute the crypto side of the trade, and a connected fiat channel-an exchange account, card program, or local off‑ramp-pushes the resulting currency to your bank. In countries where regulated partners are available, those entities handle the bank transfer itself while SimpleSwap focuses on routing, pricing, and status transparency. In P2P arrangements, there's also a human buyer who wires money directly to you, usually under the watch of an escrow system.

Understanding who touches your funds, and in what order, is more than just theory. It tells you where KYC checks will happen, which party sets fees, who can help if something gets stuck, and how much counterparty risk you're really taking on with any given USDT‑to‑bank route.

Main Ways to Withdraw USDT to a Bank Account

Using centralized exchanges (CEX)

For most people, the first workable path from USDT to a bank is a centralized exchange. The flow is straightforward: you send USDT from your wallet to the exchange, trade it into a fiat balance such as USD or EUR, and then request a withdrawal to your bank via SEPA, SWIFT, ACH, or another local rail. Because these platforms publish fee schedules and show live order books, it's usually easy to see the rate you're getting and the fees you'll pay before you hit "confirm."

That transparency is the upside. The trade‑off is that CEXs almost always require KYC and often limit which countries and currencies they'll support for direct bank withdrawals. Some users are also uncomfortable keeping large balances on a single exchange, whether for security reasons or just policy risk. That's where SimpleSwap often comes in as a companion tool rather than a replacement. Instead of forcing you to manage full trading interfaces on multiple venues, it lets you convert USDT into the asset or network that a given exchange or off‑ramp handles best, then you use that venue purely for the last‑mile bank transfer.

P2P platforms and marketplaces

In countries where banking rails into and out of crypto are thin, peer‑to‑peer USDT sales have turned into an important workaround. On these marketplaces, you post an offer to sell a certain amount of USDT, and a buyer agrees to pay you in local currency-usually by bank transfer, mobile wallet, or another familiar channel. A good P2P platform holds your USDT in escrow while the buyer sends the money. Once you confirm that the fiat has really landed, the escrow releases the USDT to the buyer.

Done right, this can unlock local currencies and banks that big exchanges ignore. But you're also taking on more hands‑on risk. You have to watch for forged payment screenshots, buyers who push you to chat off‑platform, and offers that look too good to be true. SimpleSwap's view on this is pragmatic: P2P can be genuinely useful where formal off‑ramps don't exist, but you should treat it like meeting a stranger to do a cash deal.

Stick to platforms with strong reputations, visible KYC, and clear dispute processes, and lean on USDT escrow features instead of trusting one‑off arrangements.

Crypto cards and third‑party payment services

Another route avoids a big one‑time withdrawal altogether. Crypto cards and payment apps let you load USDT (or other coins), then quietly convert it in the background whenever you tap the card, shop online, or pull cash from an ATM. From your point of view, it feels like using any other debit card. Under the hood, the provider is selling your USDT in real time and settling each purchase in whatever currency the merchant expects.

For day‑to‑day spending, that can be far more convenient than wiring a lump sum to your bank every time you need money. The cost, however, is usually spread across card fees, FX spreads, ATM charges, and sometimes weekend or "high‑volatility" mark‑ups.

Local off‑ramp services and partners

In some markets-especially where businesses move significant size-dedicated off‑ramp providers and OTC desks sit at the center of USDT cash‑outs. Their job is to take in larger USDT sums, convert them into local currency, and route that money through domestic banking rails under clearly defined terms. Typical clients include companies paying suppliers, payroll operations, and high‑net‑worth individuals who need to move size without fighting retail limits on exchanges.

Fees Explained: What You Really Pay When Cashing Out USDT

Types of fees involved

When people ask how to withdraw USDT to a bank account, they usually look at a single line on a fee page and stop there. In reality, you're dealing with a stack of costs. The first layer is the blockchain itself: every USDT transfer pays a network fee to validators or miners. On some chains that's barely noticeable; on others, especially when markets are busy, it can spike enough to make small withdrawals pointless.

Then comes the conversion cost. When you trade USDT into fiat, the platform or off‑ramp earns money either through an explicit commission, a spread baked into the exchange rate, or both. A fraction of a percent may not sound like much, but on a five‑ or six‑figure withdrawal it adds up quickly. On top of that, many services charge a separate fee just to send fiat to your bank-sometimes a flat amount, sometimes a percentage, sometimes a mix.

Finally, there are the "invisible" charges on the banking side. Incoming wires can carry fixed fees or get shaved by correspondent banks along the route. If your withdrawal involves a currency conversion, your bank or payment processor may apply its own FX spread as well. SimpleSwap's view is that you only see the real price of a USDT cash‑out when you add all of these layers together: blockchain fee plus trading cost plus payout and banking friction.

How fees vary by method and network

The chain you choose for moving USDT can completely change your cost structure. TRC20 transfers on TRON are often cheap and consistent, which is why so many exchanges lean on them for day‑to‑day withdrawals. ERC20 transfers on Ethereum, by contrast, can swing from reasonable to painfully expensive depending on congestion, making them better suited to fewer, larger moves rather than lots of small ones. Other networks sit somewhere in between, with their own patterns for price and speed.

The off‑ramp method matters just as much. A classic CEX setup might offer tight trading spreads and then charge a flat bank withdrawal fee (which is great if you're moving $10,000, less so if you only need $200). P2P trades may advertise "zero fees" yet hide their costs inside wide USDT‑to‑fiat spreads and higher counterparty risk. Crypto cards bundle everything into FX margins, ATM fees, and card charges. OTC desks often quote custom rates that improve with size.

Estimating your real cash-out cost before you withdraw

Before you push any "withdraw" button, it's worth doing a quick sanity check on the numbers. Start with how much USDT you plan to cash out. Apply the current USDT‑to‑fiat rate and subtract the trading or platform fee the service quotes. From that subtotal, factor in the network fee for sending USDT, any fiat withdrawal or card charges, and what your bank is likely to take in wire and FX costs.

That back‑of‑the‑envelope "USDT to bank calculator" immediately shows whether a given route makes sense-or whether you should change networks, combine several smaller withdrawals into one, or pick a different off‑ramp altogether.

Withdrawal Limits, KYC, and Compliance Requirements

Platform limits and verification tiers

If you've ever tried to move a larger amount of USDT and suddenly hit a "withdrawal limit," you've already met the KYC system at work. Every serious exchange, card issuer, or off‑ramp ties its limits to how well it knows you. At the lowest tier (an email and maybe a phone number), you'll usually see tight daily caps suited to testing the system, not running a business.

As you submit more information - government ID, proof of address, occasionally source‑of‑funds - those ceilings rise. Fully verified users can generally move meaningful size, though the numbers still reflect each platform's risk appetite. SimpleSwap designs its flows around that reality.

It assumes the exchanges and payment partners on the fiat side will only process larger USDT‑to‑bank transfers for customers who have cleared the appropriate checks. That alignment helps protect you from abrupt freezes and "manual review" surprises, because the crypto leg of the transaction is being built with realistic off‑ramp limits in mind. Understanding where your own account sits in this hierarchy lets you plan withdrawals instead of finding out, mid‑cash‑out, that you're stuck at a lower tier.

Bank and regulatory constraints

Even if your crypto provider is ready to send money, your bank and local regulators still have a say. Banks are under pressure to understand where funds come from, and "proceeds of USDT sales" is a phrase that tends to draw extra attention. Some institutions simply log the transaction and move on; others apply stricter monitoring to frequent or high‑value crypto‑linked inflows, especially when they cross borders.

Rules also shift from one jurisdiction to another. A USDT withdrawal that sails through in one country might trigger enhanced due‑diligence somewhere else, purely because the local supervisor expects banks to be more conservative with crypto. SimpleSwap can't give legal advice or interpret your local law, but it builds its processes so that partner payouts leave a clear, auditable trail.

Planning ahead for larger withdrawals

The bigger your cash‑out, the less it should feel like a spur‑of‑the‑moment decision. Moving significant USDT in one go can require higher KYC tiers, advance notice to your bank, or even a different channel altogether, such as an OTC desk that specializes in regulated large‑ticket flows. Treating a major withdrawal like any other transaction is how people end up with funds in limbo while multiple teams review the same transfer.

Plan big crypto transactions like you would any other major financial move. Well before you send USDT, talk to support at the platforms involved, outline the amounts and timing you have in mind, and ask what documentation they'll need. In many cases, SimpleSwap can coordinate with its partners so the crypto conversion, OTC leg, and final bank transfer are aligned.

That preparation doesn't just reduce the risk of delays or freezes; it gives you room to structure the withdrawal (whether as one payment or several staged ones) in a way that fits platform limits, your bank's comfort level, and your own risk tolerance.

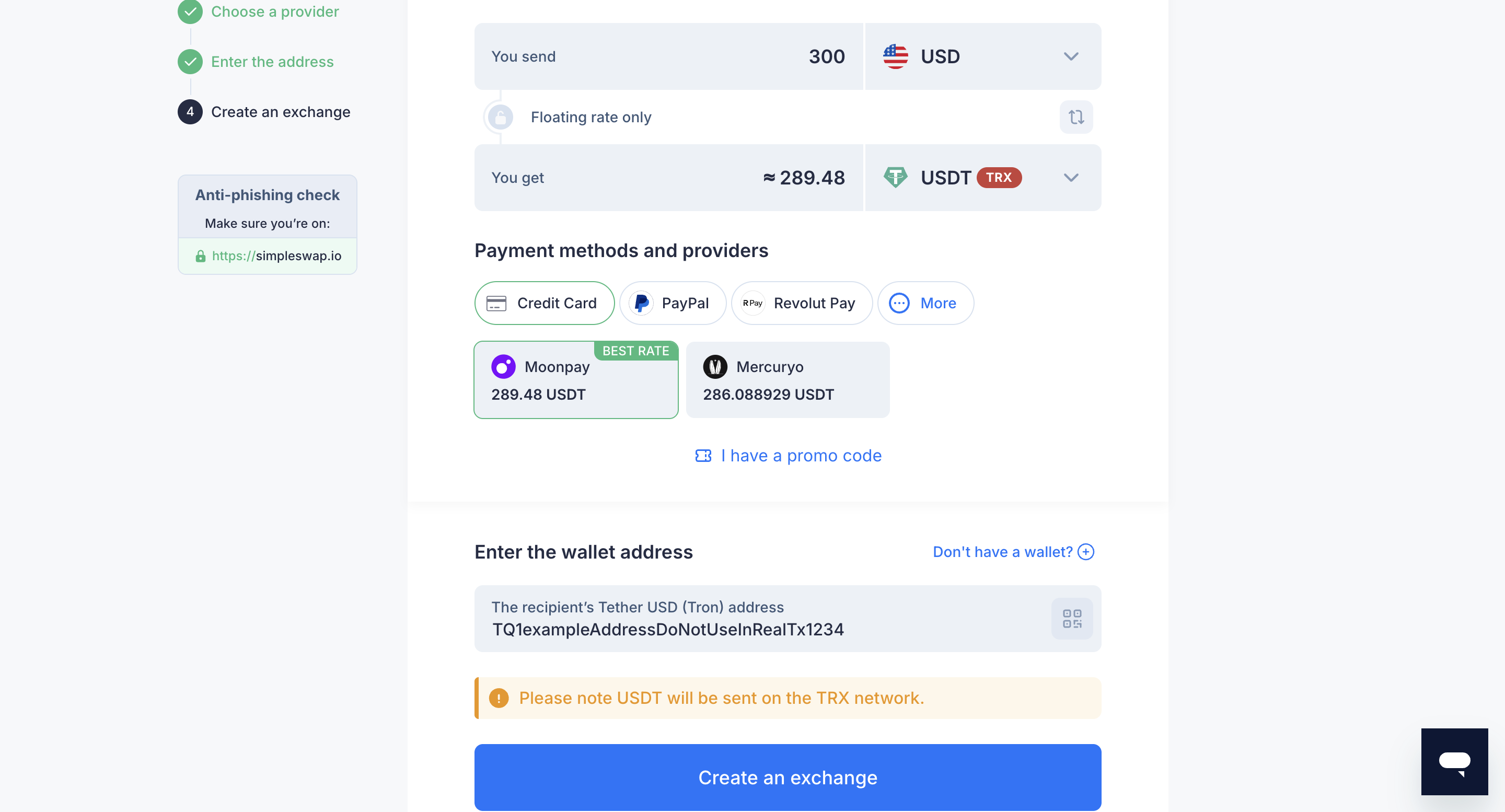

Step-by-Step Process: Withdrawing USDT to a Bank Using SimpleSwap

Quick Start: Buy, Stake, and Farm

Buy coins on SimpleSwap

Here’s how it is done on SimpleSwap (as seen with buying USDT):

1. Open SimpleSwap and choose Buy/Sell Crypto.

2. In You Send, pick your coin (for example, USD/BTC/ETH). In You Get, select USDT, or any other coin of your choosing. Click Exchange.

3. Add exchange details

Choose your payment method, paste your receiving address (so funds land where you’ll use them), and click Create an exchange.

4. Receive your USDT (typically within minutes) – no registration required.

Once USDT crypto arrives, keep a small buffer for gas and you’re ready for dApps, staking (delegation), or bridging.

Staking Basics

Choose a crypto network and validator with strong uptime and reputation.

Delegate from your wallet, confirm any lock-ups, and track reward frequency.

Yield Farming Basics

Select one of the vetted yield farming platforms and a liquidity pool with healthy volume and depth.

Add liquidity, receive LP tokens, and stake LP in the farm if required.

Harvest and compound on a schedule that fits your fee budget.

Risk Management and Safety Best Practices

Avoiding scams and chargeback risks

As USDT has gone mainstream, it has also become a favorite playground for scammers, especially in P2P deals and informal Telegram‑style channels. The patterns repeat: buyers insist on chatting off‑platform, pressure you to release USDT before your bank shows cleared funds, dangle rates that are far above market, or send screenshots of transfers that never really happened. In some countries, chargebacks are another headache - someone pays you with a reversible method, gets your USDT, then disputes the payment with their bank or card issuer.

Operational hygiene: addresses, networks, and test amounts

Most permanent USDT losses don't come from sophisticated hacks; they come from simple, avoidable mistakes. Typing an address by hand and swapping two characters. Selecting ERC20 in your wallet and TRC20 on the receiving platform. Sending your whole balance in one shot to a destination you have never tested before. None of this feels dramatic at the time, but the outcome can be funds that are very hard-or impossible-to recover.

SimpleSwap tries to normalize a few basic habits. Always copy‑paste addresses from the interface, then visually check the first and last characters. Always make sure the network you pick while withdrawing is the same one the recipient expects, and never assume an exchange will magically credit funds sent on the wrong chain.

And when you're dealing with a new destination, send a small test amount first. If that test arrives quickly, with the right amount and on the right balance page, you've just de‑risked the larger transfer that follows. Over time, this kind of operational hygiene turns into muscle memory and dramatically lowers the odds of a catastrophic error.

Working with your bank proactively

Even if your crypto setup is flawless, the bank at the end of the line can still introduce friction. Some institutions are comfortable with compliant crypto inflows; others are wary, slow, or simply inconsistent. If your first serious USDT cash‑out shows up as an unexplained international wire with a vague reference, it's not surprising if a compliance team wants to ask questions.

A little advance work with your bank goes a long way. Reading its public stance on crypto‑related transfers, or even calling to ask what kind of documentation they might need, helps you avoid surprises. When you do withdraw, having a clean package of records (swap confirmations, transaction hashes, partner payout receipts) makes it much easier to demonstrate a clear, legitimate path from USDT on a blockchain to fiat in your account. That, in turn, reduces the risk of frozen transfers, awkward account reviews, or urgent requests for "source of funds" explanations right when you need the money most.

Optimization Tips: Saving on Fees and Time

Choosing the right network and timing

For most people, the "cheapest way" to withdraw USDT isn't about finding a secret low‑fee platform, but about picking the right network and sending at the right moment.

Each USDT network has its own personality. Some chains are designed for low, predictable fees and handle small, frequent withdrawals well. Others become expensive when markets are busy but are perfectly fine if you move larger amounts less often. Fee conditions in 2025 can still swing quickly around big news, liquidations, or new token launches, so assuming that today will look like yesterday is an easy way to overpay.

Speed is the other half of the equation. A bargain‑price network isn't much use if it regularly clogs when you're trying to move funds in a hurry. In some situations, like covering a bill with a fixed deadline, it can be worth paying a few extra dollars on chain simply to lock in fast confirmations and peace of mind.

Structuring withdrawals to match limits and goals

Even after you pick a route and a network, how you break up your withdrawals still matters. Flat fees from banks and processors usually favor fewer, larger transfers: paying a $20 wire fee once on $10,000 hurts a lot less than paying it five times on $2,000. Percentage‑based fees behave differently-they scale with volume-so in those cases combining or splitting might not change the total quite as dramatically.

Account limits and compliance behavior sit on top of that. Your current KYC tier may cap how much you can move in a single day or per transaction, forcing you to stage withdrawals over time. On the banking side, a long string of small, repetitive crypto‑linked inflows can attract just as much attention as one very large payment that doesn't fit your usual pattern.

Tax and Reporting Considerations

How USDT cash‑outs are typically treated

In most jurisdictions, converting USDT to fiat is a taxable event or at least a reportable one. The details vary-some authorities focus on the gain between your USDT acquisition cost and what you receive in fiat; others look at the full transaction history from the original crypto purchase to the final cash‑out.

What matters for you as an investor or business is that a USDT withdrawal is rarely invisible from a tax perspective. If you've moved between several coins before ending up in Tether, those prior swaps may already have created realized gains or losses, long before you touch your bank account.

Record‑keeping best practices

USDT users often underestimate how quickly transaction histories grow, especially if they are active traders or use multiple networks. Waiting until tax season to "figure it out" usually ends in a painful hunt through explorers, CSV exports, and email confirmations.

A more efficient approach is to:

Tag major events as they happen - large buys, big swaps, and withdrawals to the bank. Keep a short log with dates, amounts, and counterparties.

Export data regularly - from wallets, SimpleSwap, and any exchanges you use. Store those files securely with meaningful filenames.

Note fiat equivalents at the time of key swaps - many tax tools need values in your local currency on specific dates.

This discipline doesn't just help with compliance. It also gives you a clearer picture of your true performance: how much profit actually made it from USDT into your bank after all fees and taxes.

Always check rules in your country and, where possible, run your records past a professional who understands both crypto and local regulations. Aligning SimpleSwap's clean transactional data with professional tax guidance is the safest way to make sure your USDT cash‑outs don't create surprises later.

Key Takeaways and Practical Checklist

Withdrawing USDT to a bank account is no longer exotic-it's a routine part of how traders, investors, and crypto‑paid professionals manage cash flow. But it's still a multi‑step process that crosses two very different systems: blockchains and banks.

Core principles to keep in mind:

You can't send USDT directly to a bank; you need a conversion layer and a fiat rail.

Total cost = network fees + trading/spread + payout fees + banking/FX friction.

Limits and KYC tiers on both crypto platforms and banks shape what's realistically possible.

Operational mistakes (wrong network, wrong address) are the most common source of permanent loss.

Clean records turn potential compliance and tax headaches into routine admin.

Before you cash out USDT, run through this quick checklist:

Confirm networks: know exactly which chain your USDT is on and which chain SimpleSwap and any partners expect.

Verify accounts: make sure your exchange/off‑ramp and bank accounts are KYC‑approved and active, with matching legal names.

Compare routes: on SimpleSwap, test a couple of paths and networks to see which combination offers the best net result for your size and timeline.

Test first: send a small USDT amount to the destination to confirm addresses, networks, and typical timing.

Document everything: save blockchain hashes, SimpleSwap confirmations, partner payout receipts, and bank statements.

Plan size and frequency: structure withdrawals around platform limits, bank comfort, and your own fee and tax efficiency.

Used thoughtfully, SimpleSwap becomes the reliable "bridge" between your on‑chain USDT and real‑world spending power-letting you move from crypto balance to bank balance with clear costs, visible status, and fewer unwelcome surprises.

FAQ

Can I send USDT directly to my bank account?

Bank accounts cannot hold crypto directly, so you cannot send USDT straight to your bank the way you send a wire or ACH. Instead, a service such as an exchange, off‑ramp, or SimpleSwap plus partners must receive your USDT, sell it for fiat, and then issue a bank transfer in your local currency.

Think of it as two steps: on‑chain transfer, then traditional payment into your bank. Every USDT cash‑out you see advertised ultimately follows this pattern, even if the app hides the complexity.

How long does a USDT withdrawal to a bank usually take?

The crypto leg is typically fast: once your USDT transaction confirms on‑chain and the swap completes, the fiat side can start. Banking speed then depends on method and region. Domestic payouts and modern instant‑payment systems can arrive within minutes or hours. Classic international wires may take one to three business days, sometimes longer around weekends or holidays.

If your transfer hits compliance checks at a bank or payment processor, additional verification can extend timelines.

Which USDT network is best for withdrawing to a bank?

No single network is "best" for everyone; it depends on fees, speed, and what your chosen platforms support. TRC20 on TRON is often cheaper and predictable for frequent or smaller transfers. ERC20 on Ethereum generally offers strong liquidity but can be expensive during congestion, making it better suited to larger amounts where network fees are a smaller percentage.

Why did I receive less money than expected in my bank?

The gap usually comes from layered fees and FX effects. First, your USDT is converted to fiat at a specific rate that may include trading spread. Then network fees, platform commissions, and withdrawal or payout fees reduce the amount sent to your bank.

If there is a currency conversion on the banking side, your bank or correspondent banks may apply their own FX spread or fixed charges.

Is withdrawing USDT to a bank taxable?

In many jurisdictions, converting USDT to fiat is treated as a taxable disposal of a digital asset, even though USDT is "stable." Any difference between your acquisition cost and the value at cash‑out can create a gain or loss. You may also need to report large transfers for transparency reasons.

What is the safest way to test a new withdrawal route?

When using a new combination of wallet, SimpleSwap route, and off‑ramp, start with a small test transaction. First, double‑check that the USDT network and address are correct and supported. Then send a modest amount, confirm it arrives, completes the swap, and successfully reaches your bank. Compare the actual received amount with your fee expectations and timeline.

If everything matches, you can confidently repeat the process with a larger sum, knowing the technical path and compliance behavior are already proven for your profile.

What should I do if my bank blocks or questions a crypto-related transfer?

Stay calm and treat it as a compliance review rather than a personal accusation. Banks must understand the origin of funds, so be ready to provide documentation: blockchain transaction hashes, exchange confirmations, and any statements from exchanges or off‑ramps involved. Explain clearly that the money comes from legitimate USDT conversions.

If your current bank remains consistently hostile to compliant crypto inflows, consider discussing the situation with them formally or exploring more crypto‑friendly institutions that publish transparent policies on digital‑asset‑linked payments.

How does SimpleSwap fit into the USDT-to-bank process?

SimpleSwap acts on the crypto side of the bridge. You send USDT to SimpleSwap on a supported network, the service converts it into the asset or route best suited for your chosen off‑ramp, and then a partner exchange, card program, or payment processor handles the actual fiat payout to your bank.

This lets you focus on picking efficient routes and currencies without managing complex trading interfaces yourself. SimpleSwap's role is to provide reliable liquidity, clear status tracking, and support while trusted partners manage regulated fiat settlement.